Caruso Weekend Report: July 27, 2025

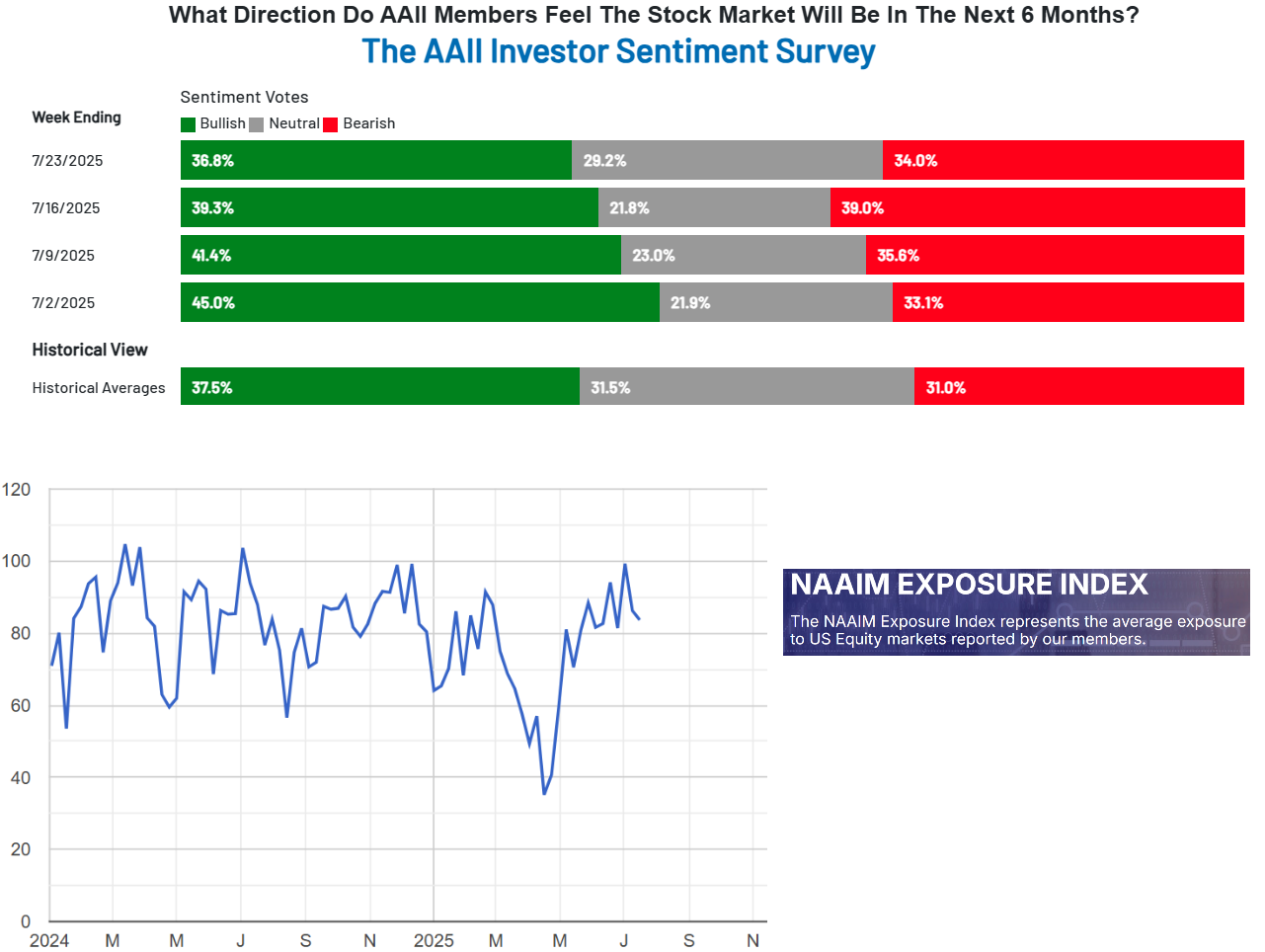

We are in the midst of an epic lock-out market rally. In a near replay of last week, the major indexes climbed steadily higher while leading groups powered ahead. Interestingly, despite the gains and chatter about “euphoria,” both the National Association of Active Investment Managers (NAAIM) exposure index and the AAII Sentiment Survey of retail traders fell for the third and second consecutive weeks, respectively. Hardly the look of a euphoric market.

We’ve been bullish for weeks, and the headline indexes have marched higher—but the broad market hasn’t kept pace. Small- and mid-cap stocks are still flat on a one-year basis. Over the weekend, we got news of a major EU-US trade deal. Combined with recent progress on a China-US deal, that development all but removes the Fed’s main excuse for delaying rate cuts.

This sets up a near-perfect repeat of the 1995 playbook we discussed in detail last week: the Fed cutting rates at all-time highs, right in the middle of a tech revolution. The market has been sniffing this out for months—just look at the relative strength in rate-sensitive themes:

- Lending (UPST)

- Crypto (IBIT, ETHA)

- Housing (Z, RKT)

If the 1995 precedent holds, we’re only at the start of a broad, sustained rally. Buckle up.